A pigmy collection app replaces the ticketing machine an agent has traditionally carried door to door. Instead of a physical device that stores data locally and syncs with the bank at the end of the day, the agent records each deposit on a phone, and the entry reaches the server in real time.

That single change is where most of the difference between manual and digital collection comes from.

What Is Pigmy Collection?

Pigmy collection is a daily deposit scheme built around small, regular savings. An agent visits a depositor, usually a daily wage earner, small trader, or farmer, collects a small amount, and issues a receipt. Over time, this builds a savings habit for people who would otherwise have no structured way to save.

The scheme has traditionally run through co-operative societies, microfinance institutions, and, in earlier decades, nationalized banks. Most of these organizations still depend on the same agent-and-machine model that has been in use for decades.

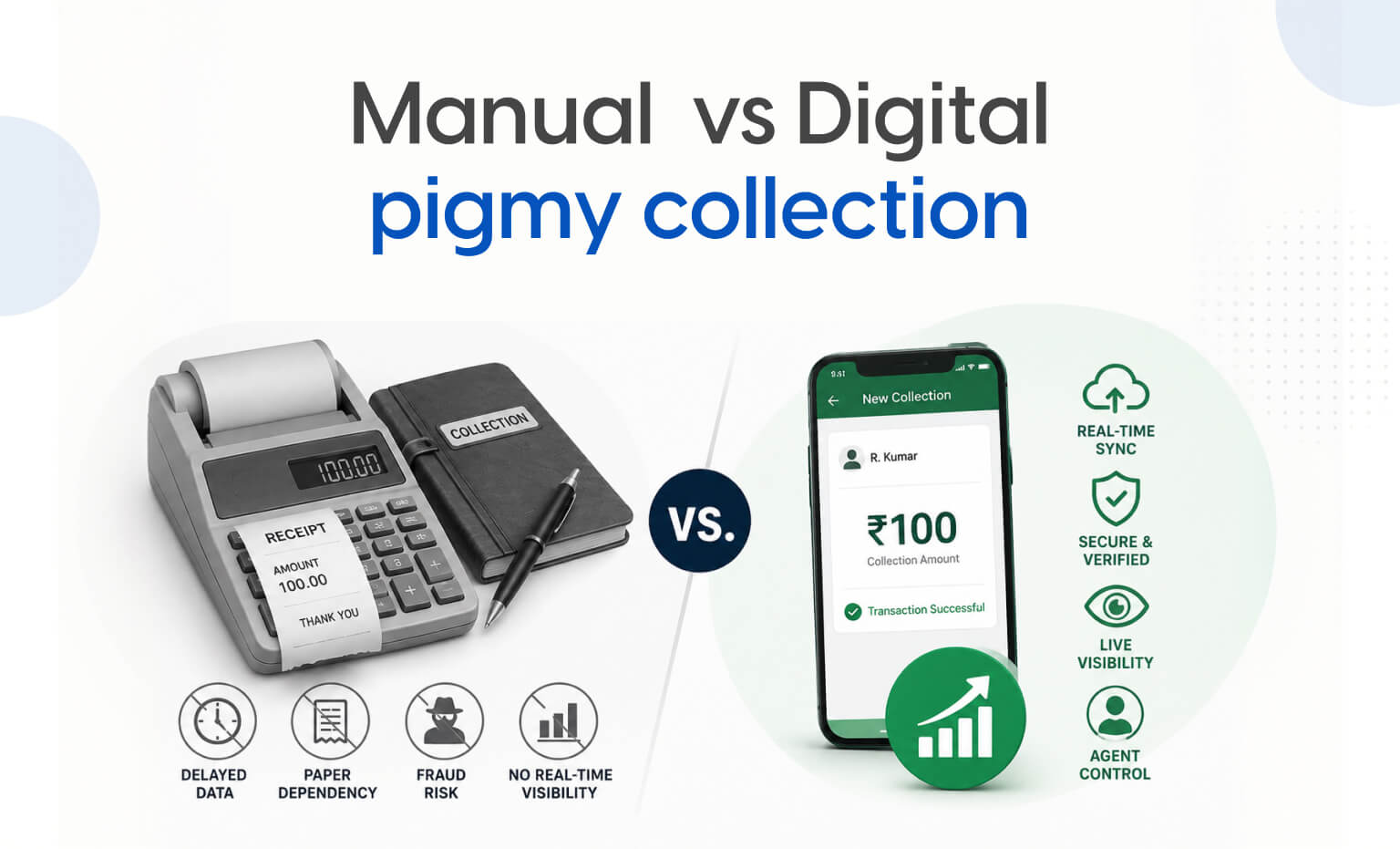

How Manual Pigmy Collection Works

The conventional process runs through a ticketing machine, and it follows the same sequence every day:

The agent visits the depositor and enters the transaction on the machine.

The machine prints a physical receipt on the spot.

At the end of the collection round, the agent returns to the branch and connects the machine to the bank’s system to upload the day’s transactions.

Every step in that sequence is a point where something can go wrong, and none of it happens in real time.

Where the Ticketing Machine Model Breaks Down

Organizations that still run pigmy collection on ticketing machines run into a consistent set of problems, and they show up regardless of the size of the operation:

High upfront cost. Ticketing machines are expensive to procure and expensive to maintain over their working life.

Delayed data. Transactions only reach the bank’s system once the agent returns and syncs the device, so admins have no real-time view of collections happening in the field.

Limited fraud control. Because data sits on the machine until end-of-day sync, there is a window where entries can be altered or misreported before anyone at the branch sees them.

Paper dependency. Every receipt is printed, which adds material cost and gives the organization no digital record unless someone manually re-enters it later.

No control over agents in real time. Admins can’t activate, block, or monitor an agent mid-day. Issues surface only after the fact.

None of these are edge cases. They are the default behavior of a system built for a pre-cloud era, still running inside organizations that now need real-time financial data to operate.

What Changes When Collection Is Digitized

Digitizing pigmy collection doesn’t change what the agent does in the field. It changes what happens to the data the moment it’s collected.

A digital collection system typically addresses the same failure points in the same order:

Transactions sync to the server as they happen, not at end of day, giving admins a real-time view of collections across every agent.

Offline data entry allows agents in low-connectivity areas to keep working, with automatic sync once connectivity returns.

Authentication and encryption apply to every transaction, closing the window where manual entries could be altered before reaching the branch.

Admins can activate, block, or reassign agents immediately, rather than waiting for an end-of-day reconciliation to catch a problem.

Multi-branch visibility becomes possible from a single dashboard, instead of each branch working off its own machine data.

The receipt can still be printed at the point of collection if the organization needs one. What changes is that the transaction no longer waits for a physical device to be walked back to a branch before anyone can see it.

The Underlying Shift

The manual model was built around a constraint that no longer exists: the assumption that field data has to be carried back physically before it can be acted on. Once that constraint is removed, most of the operational cost of running pigmy collection, hardware, reconciliation time, fraud exposure, delayed visibility, goes with it.

For co-operative societies and microfinance institutions managing distributed agent networks, that’s not a minor efficiency gain. It’s the difference between finding out about a problem the next morning and finding out about it while it’s still happening.

Want to see how this plays out in practice? Read the full Pigmy Plus story on our blog.